You are here

Feed aggregator

Avenir en sélection, erreurs défensives, supporters en colère… ce que Mandi a confié après l’élimination

Joueur le plus capé de l’histoire des Fennecs, Aïssa Mandi a encaissé l’élimination face à la Suisse (2-0) avec la même amertume que ses coéquipiers. […]

L’article Avenir en sélection, erreurs défensives, supporters en colère… ce que Mandi a confié après l’élimination est apparu en premier sur .

Categories: Afrique, European Union

Sept jours et des millions de personnes en deuil : à quoi s'attendre aux funérailles de l'ancien guide suprême iranien Ali Khamenei

Les « funérailles du siècle » de l'ancien guide suprême iranien, l'ayatollah Ali Khamenei, débutent à Téhéran ce vendredi 3 juillet, plus de quatre mois après son assassinat.

Sept jours et des millions de personnes en deuil : à quoi s'attendre aux funérailles de l'ancien guide suprême iranien Ali Khamenei

Les « funérailles du siècle » de l'ancien guide suprême iranien, l'ayatollah Ali Khamenei, débutent à Téhéran ce vendredi 3 juillet, plus de quatre mois après son assassinat.

Categories: Afrique, Határon túli magyar portálok összesített hírei

European Parliament Plenary Session – July 2026

Written by Clare Ferguson with Áine Feeney.

As Members gather for the last plenary session before the summer recess, their agenda covers enlargement, foreign affairs, competitiveness, the EU budget, agriculture, social security and the environment. On Tuesday morning, a debate will follow a presentation of the programme of activities of the Irish Presidency of the Council of the European Union, which began on 1 July. On Wednesday morning, Members will hear Council and European Commission statements on the conclusions of the European Council meeting of 18‑19 June 2026.

EU-Mexico relationsBilateral relations between the EU and Mexico have been bolstered by the current framework since 2000. On Tuesday, Parliament is due to decide whether to give its consent to the conclusion of two instruments to update this framework, the EU-Mexico Political, Economic and Cooperation Strategic Partnership Agreement (Modernised Global Agreement, MGA) and an interim Trade Agreement (iTA), both of which were signed by the EU and Mexico in May 2026. Parliament remains in favour of modernising the MGA, with a joint report by the International Trade (INTA) and AFET committees welcoming it as a step towards further economic expansion that could benefit EU companies and farmers. The INTA committee is due to vote on a draft recommendation on the conclusion of the iTA before the plenary vote.

Passenger rightsLower ticket prices and a wider choice of routes are not the only results of air transport liberalisation. On Monday, Members are expected to discuss an agreement to revise the air passenger rights framework to better protect passengers during increasingly common travel disruption. Delayed in the Council for over a decade, Parliament has shown consistent support for measures to protect air passengers and their rights. Parliament negotiators reached a political agreement in conciliation with the Council in June 2026. The agreement maintains the three-hour threshold for compensation for flight delays and strengthens passenger rights including on rerouting options, protection for missed connections and reimbursement for unused vouchers.

Social security when working abroadA reform of EU social security rules aims to help citizens living or working in another EU country and better distribute responsibilities between EU countries. Members are set to vote on a provisional agreement on the move to modernise the rules on Monday. Parliament’s negotiators maintained mandatory prior notifications for the construction sector in the agreed text, meaning that authorities of the home Member State would be notified if someone works in another Member State. Parliament’s Committee on Employment and Social Affairs (EMPL) confirmed the agreement in April 2026 and Parliament and the Council now need to formally adopt the new social security rules.

East Asia relationsThe geopolitical situation in East Asia has grown more volatile as the region experiences increased security challenges triggered by authoritarian regimes. On Monday evening, Members are expected to vote on an AFET committee recommendation, which affirms the need to deepen cooperation with partners in the region, including Japan, Korea, ASEAN and Taiwan. Parliament also recommends establishing a comprehensive EU-Taiwan cooperation framework, in addition to strengthening EU engagement with regional security initiatives and diplomatic efforts to prevent further escalation in East Asia.

Fertiliser pricesThe crisis in the Middle East and the closure of the Strait of Hormuz has caused an increase in fertiliser prices, placing a significant financial burden on farmers. On Tuesday, Members are set to vote on a proposal for a regulation to provide temporary common agricultural policy (CAP) support, which would offer exceptional support to farmers most affected by the soaring prices, including the possibility of increased advances on direct payments through existing CAP envelopes. Given the urgency, Parliament decided to consider the proposal without preparing a report, to enable farmers to make prompt decisions on buying fertilisers for the year ahead.

28th tax regimeThe EU’s plans to allow companies to register as an ‘EU Inc.’, recognised across all Member States, under a ’28th regime’, are central to its competitiveness agenda, aimed at simplifying rules for companies to scale up in the single market. Complementing the legislative proposal already on the table, Members are expected to vote on an own-initiative report from the Committee on Economic and Monetary Affairs (ECON), on Thursday, on the feasibility of a 28th tax regime and its potential to support competitiveness by simplifying and harmonising corporate taxation.

Environmental crimeEnvironmental crimes can have a devastating impact, yet they are difficult to detect and prosecute. Parliament has repeatedly called for measures to combat such crimes. On Wednesday, Parliament is scheduled to vote on endorsement of the EU’s ratification of the Council of Europe’s new Convention on the Protection of the Environment through Criminal Law. A report from the Legal Affairs (JURI) Committee recommends ratification, concluding that the convention is consistent with the EU directive. The new convention establishes minimum requirements for the criminalisation of environmental offences related to activities such as pollution, destruction of biodiversity and improper handling of hazardous waste.

EU BudgetTo enter a 2025 budget surplus of €2.1 billion as revenue in the 2026 budget, on Tuesday Parliament is set to consider the Council’s position on draft amending budget No 1/2026 (DAB 1/2026). While endorsing the proposal, a report adopted by the Committee on Budgets (BUDG) welcomes that higher own resources are driving the surplus rather than underspending, but reiterates its long-standing view that revenue from fines and fees should strengthen the EU budget instead of lowering national contributions, and calls for more sustainable EU own resources in the next multiannual financial framework.

Annual enlargement reportsEnlargement remains a prominent topic at this plenary session. On Tuesday, Members are expected to debate separately three reports prepared by the Committee on Foreign Affairs (AFET), on Ukraine, Moldova and Serbia. The report on Ukraine stresses the need for a ‘sustainable’ ceasefire and a peace agreement reached with the participation of the EU, while also recognising Ukraine’s European integration as a strategic priority for the Union.

AFET’s report on Moldova commends the country’s commitment to EU accession, condemning attempts by Russian efforts to destabilise Moldova’s path to accession through interference campaigns.

As a result of political instability in the country, Serbia’s EU accession process remains at an impasse. The AFET report recalls that accession is conditional on respect for EU values and democracy, reiterating the need for Serbia to affirm its geopolitical orientation towards the EU, particularly in the context of Russia’s war of aggression against Ukraine.

Further reading- Agenda

- Priority dossiers under the Irish EU Council Presidency

- 2025 Commission report on Ukraine

- 2025 Commission report on Moldova

- 2025 Commission report on Serbia

- EU-Mexico agreements

- The changing geopolitical situation in East Asia

- Temporary CAP support to help farmers cope with high fertiliser prices

- Feasibility of a 28th tax regime and its potential to support EU competitiveness

- Air passenger rights

- Developments in social security coordination

- EU accession to the Council of Europe Convention on Environmental Crime

- Draft amending budget No 1/2026: 2025 surplus

Categories: Balkans Occidentaux, European Union

Beyond Fragmentation: Legal Instruments, Capital Markets and the Governance of the EU Single Market

This Policy Paper examines the renewed debate on completing the EU Single Market. It argues that the challenge is not simply to adopt more EU legislation or to choose between regulations and directives, but to turn formal market access into operational market integration. Focusing on capital markets, services and governance, the paper shows that fragmentation persists when legal convergence is not matched by implementation capacity, supervisory alignment and political incentives for compliance. Completing the Single Market means making Europe the natural scale for firms, capital and innovation.

Read here in pdf the Policy Paper by Dr Apostolos Samaras, Research Fellow, European Programme ‘Ariane Condellis’, Hellenic Foundation for European and Foreign Policy (ELIAMEP).

Introduction: From Single Market Completion to European Scale“All those who, in trying to meet the economic challenges set out by the treaty of Rome, neglected the political dimension have failed. As long as [those] challenges will be addressed exclusively in an economic perspective, disregarding their political angle, we will run – I am afraid – into repeated failures”

Paul-Henri Spaak, Discours à la Chambre des Représentants, 14 June 1961.

To date the Single Market is the EU’s most significant economic achievement. However, its relevance depends on its ability to support European competitiveness under rapidly changing global conditions. In January 2025, the European Commission unveiled the so-called “competitiveness compass”, a fresh strategy aimed at revitalising EU’s dynamism (European Commission, 2025a). The Commission views competitiveness as a multifaceted concept, structured around several crucial elements including the functioning of the Single Market, access to capital, innovation, skills and infrastructure (European Commission, 2024). Within this framework, a well-functioning internal market is presented as a central condition for enabling businesses to scale, facilitating investment and supporting productivity growth across the EU.

The European Commission has consistently identified hurdles affecting the functioning of the Single Market, particularly in services and areas requiring administrative coordination (European Commission, 2020a). The aforementioned barriers increase costs for businesses, reduce legal certainty and discourage cross-border activity. Moreover, recent policy reports place these issues in a broader economic context. Draghi (2024) links Europe’s investment gap to structural inefficiencies, including fragmentation within the Single Market. Letta (2024) similarly argues that the Single Market must evolve to support scale, speed and strategic resilience. Institutional policy analysis reinforces this assessment, e.g. the International Monetary Fund (IMF) notes that Europe’s growth potential is restrained by weak productivity and limited scale (IMF, 2024).

The European Council has endorsed a renewed focus on the Single Market as a key driver of competitiveness, emphasising the need to remove barriers and improve its functioning.

These findings are indicated in current EU political priorities. The European Council has endorsed a renewed focus on the Single Market as a key driver of competitiveness, emphasising the need to remove barriers and improve its functioning (European Council, 2026). Market fragmentation is affecting investment decisions, innovation, productivity growth and the global position of European businesses, also having broader strategic implications. As recent policy analysis emphasises, the absence of an integrated internal market limits businesses’ ability to scale and raises capital costs, weakening Europe’s position in an increasingly bloc-based global economy, where size and coordination determine competitiveness (Jacques Delors Institute, 2026).

This paper argues that the next phase of Single Market reform should not be framed simply as a choice between more or less EU legislation. The central question is whether EU legal instruments, enforcement mechanisms and supervisory structures can convert formal market access into operational market integration. Capital markets and services show that fragmentation persists where legal convergence is not matched by administrative capacity, supervisory alignment and political incentives for compliance.

The Problem: What Kind of Fragmentation?Α precise understanding of fragmentation requires distinguishing between its main sources. Two factors are particularly relevant. The first is incomplete regulatory convergence. […] The second is implementation failure. Even where appropriate EU legislation exists, its application may still be uneven.

A precise understanding of fragmentation requires distinguishing between its main sources. Two factors are particularly relevant. The first is incomplete regulatory convergence. In certain areas, EU legislation does not fully eliminate cross-border burdens. Capital markets provide a clear example, where differences in insolvency law, taxation in cross-border investing and market infrastructure continue to create barriers to integration. The second is implementation failure. Even where appropriate EU legislation exists, its application may still be uneven. Although not confined to Single Market law, the persistence of infringement litigation before the Court of Justice of the European Union (CJEU) confirms that uneven application remains a structural problem in EU law enforcement, with 200 infringement actions brought between 2021 and 2025 (Court of Justice of the European Union, 2026). Enforcement mechanisms are often slow and reactive. The Commission has acknowledged the need to strengthen enforcement as part of its broader strategy (European Commission, 2022).

At a deeper level, fragmentation signifies a structural trade-off. Greater market integration entails constraints on national regulatory autonomy, especially in areas such as finance, taxation or supervision.

Moreover, Member States apply EU law within national systems shaped by domestic institutional structures and policy priorities. This can create incentives to preserve regulatory discretion or to delay reforms, particularly in politically sensitive areas, even where legal obligations are clear. At a deeper level, fragmentation signifies a structural trade-off. Greater market integration entails constraints on national regulatory autonomy, especially in areas such as finance, taxation or supervision. The extent to which this trade-off is genuinely accepted varies across Member States and over time, shaping the pace and the depth of integration.

These factors can be interlinked in practice. Regulatory divergence may endure because implementation is weak, whilst domestic political incentives sometimes discourage convergence. The European Commission’s May 2025 Single Market Strategy identifies the “Terrible Ten” barriers disrupting the market, such as restrictive national services rules, long delays in standard-setting and overly complex EU rules (European Commission, 2025b). Evidence from the services sector exemplifies this dynamic. Despite existing EU legislation, barriers remain widespread, reflecting both regulatory and implementation challenges (European Commission, 2020a).

The Digital Single Market provides a useful illustration of this broader pattern. Recent analysis identifies mutually reinforcing bottlenecks: uneven regulatory implementation, nationally siloed infrastructure, barriers to data flows and skills mobility, and insufficient growth-stage finance. This confirms that Single Market reform cannot rely on legal harmonisation alone. Uniform rules must be connected to enforcement capacity, digital infrastructure, public procurement, capital market depth and practical compliance tools if firms are to scale across borders (Aarnio et al., 2026).

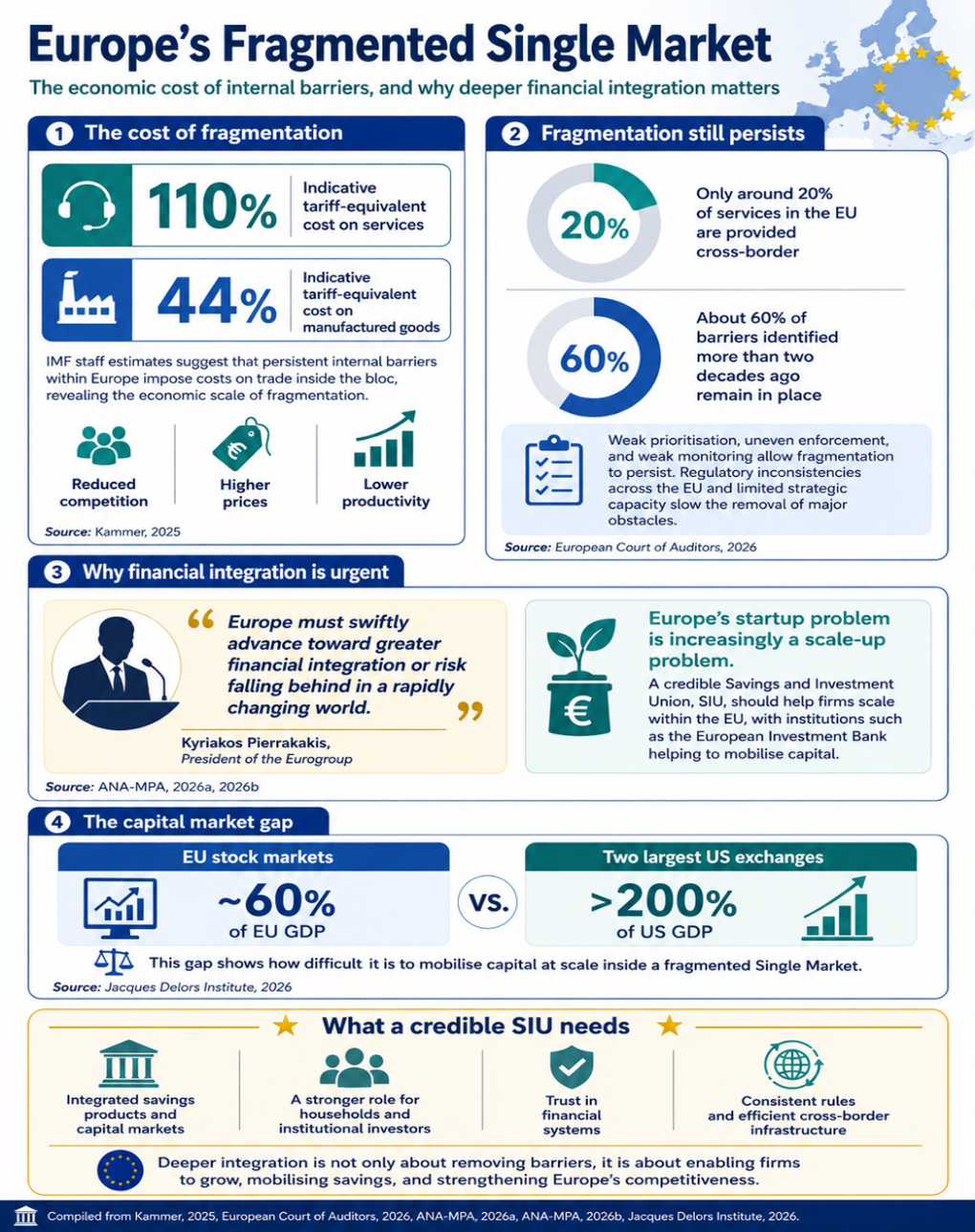

IMF staff estimates suggest that persisting internal barriers within Europe may be equivalent to an indicative 110% tariff on services and 44% for manufactured goods […] recent audit evidence finds that only around 20% of services in the EU are provided cross-border, while approximately 60% of barriers identified more than two decades ago remain in place.

IMF staff estimates suggest that persisting internal barriers within Europe may be equivalent to an indicative 110% tariff on services and 44% for manufactured goods (Kammer, 2025). This shows the economic scale of fragmentation. European consumers and businesses face these costs through reduced competition, increased prices and lower productivity. Moreover, recent audit evidence finds that only around 20% of services in the EU are provided cross-border, while approximately 60% of barriers identified more than two decades ago remain in place (European Court of Auditors, 2026). At the same time, weaknesses in prioritisation, enforcement and monitoring suggest that fragmentation persists due to regulatory inconsistencies across the bloc and limited EU strategic capacity to remove the most significant obstacles (European Court of Auditors, 2026).

A competitiveness agenda that creates startups but fails to support scaleups would leave Europe’s structural scale problem unresolved.

Kyriakos Pierrakakis, the President of the Eurogroup, has stressed that Europe faces a pivotal decision: it must swiftly advance toward greater financial integration or face the risk of falling behind in a world that is rapidly changing (ANA-MPA, 2026a). More specifically, Europe’s startup problem is increasingly a scaleup problem. Eurobarometer evidence supports the view that the Single Market should be judged not only by market access, but by its capacity to help firms grow across borders. A competitiveness agenda that creates startups but fails to support scaleups would leave Europe’s structural scale problem unresolved (European Commission, 2025c). EU innovative startups and scaleups continue to face fragmented regulatory regimes, high compliance costs, limited access to late-stage capital, skills shortages and difficulties in using cross-border procurement and institutional markets (Thomadakis & Marcus, 2025).

…EU stock markets have a combined capitalisation of roughly 60% of EU GDP, while the two largest US exchanges alone exceed 200% of US GDP

A credible SIU should therefore be judged by whether it enables firms to scale inside the EU, with institutions such as the European Investment Bank helping to mobilise capital (ANA-MPA, 2026b). It is noteworthy that EU stock markets have a combined capitalisation of roughly 60% of EU GDP, while the two largest US exchanges alone exceed 200% of US GDP (Jacques Delors Institute, 2026). This disparity highlights the structural difficulty of mobilising capital at scale within a fragmented Single Market. The SIU framing places greater emphasis on the role of households and institutional investors, as well as on the integration of savings products and capital markets. Nonetheless, mobilising savings depends on trust in financial systems, consistent regulatory frameworks and efficient cross-border infrastructure.

{kind=link}

FIGURE 1: Market barriers and the rationale for the SIU

Legal Integration and its Limits

The EU’s legislation governing the Single Market is prima facie comprehensive. It encompasses primary law provisions, specified and complemented by extensive secondary law. This common binding framework establishes directly enforceable rights for economic actors and prohibits a wide array of restrictions on cross-border activities. In that respect, EU law is sound and unavoidable.

Even though it has been established that EU legislation prohibits unjustified restrictions on the free movement of capital, services, goods, and persons, it certainly does not eliminate the conditions under which those restrictions arise.

However, the strength of EU law should not obscure its limits. Even though it has been established that EU legislation prohibits unjustified restrictions on the free movement of capital, services, goods, and persons, it certainly does not eliminate the conditions under which those restrictions arise. Nor does it ensure convergence in administrative practices, regulatory approaches or institutional capacity. These are structural limitations, since the implementation of EU law depends on national authorities that operate within different legal traditions, administrative systems and policy priorities. This leads to the familiar paradox that the same EU legal rule may produce different outcomes across Member States.

…there is increasing support for regulations (Wax & Ionta, 2026), which are binding and directly applicable, reducing the scope for divergence.

Policy debates have focused on this issue, which is also intrinsically correlated to national sovereignty concerns. Directives, as binding legal acts that allow flexibility in national transposition, granting Member States some national discretion to decide how to achieve the set objectives, have often resulted in divergent implementation. In response, there is increasing support for regulations (Wax & Ionta, 2026), which are binding and directly applicable, reducing the scope for divergence. The shift towards regulations is already visible in EU legislative practice: in recent years regulations have become the dominant instrument among legislative acts adopted under the ordinary legislative procedure (Publications Office of the European Union, n.d.). This approach aims to address possible legal confusion among Member States, without being a panacea for every problem, since ultimately all EU rules depend on national enforcement. Legal uniformity, in that sense, mitigates one aspect of market fragmentation, whilst not addressing other disparities in administrative capacity or supervisory practices.

Recent OECD evidence links regulatory compliance costs to weaker productivity and lower business dynamism.

Recent OECD evidence links regulatory compliance costs to weaker productivity and lower business dynamism (Andrews et al., 2026). This matters for the Single Market because firms experience EU law also as compliance tasks, administrative procedures and enforcement practices. Regulations can reduce one important source of fragmentation by limiting divergent national transposition, but they do not remove the practical costs of compliance. Evidence on cumulative compliance costs for SMEs shows that burdens often arise from national interpretation, monitoring and enforcement practices, as well as from the accumulation of obligations over time (European Commission, 2015). These costs may affect firms’ decisions to innovate, enter new markets or expand across borders. The implication is that the choice of legal instrument matters, but it must be accompanied by clear implementation planning, proportionate enforcement and attention to administrative capacity. Otherwise, directly applicable rules may still produce uneven market effects across Member States (European Commission, 2015; Capuano, 2025).

The increasing reliance on regulations should be treated as a governance choice, not as a shortcut to integration.

Even where EU rules are directly binding, Member States remain central to how their effects materialise for businesses and citizens (OECD, 2025). The increasing reliance on regulations should be treated as a governance choice, not as a shortcut to integration. Regulations can limit national divergence, but where they postpone application, rely heavily on implementing acts, or require substantial national administrative adjustment, they may reproduce some of the same practical problems usually associated with directives (Capuano, 2025). The question is therefore not whether regulations are preferable in abstract terms, but under what conditions they can produce uniform market effects without increasing legal complexity or weakening accountability.

Policy discussions have also explored the use of optional EU-wide legal regimes, such as the so-called “28th regime” corporate legal framework, as a means of reducing fragmentation without requiring full harmonization.

Policy discussions have also explored the use of optional EU-wide legal regimes, such as the so-called “28th regime” corporate legal framework, as a means of reducing fragmentation without requiring full harmonization (Hallak, 2026). It would allow businesses to operate under a single set of EU rules across Member States, bypassing divergent national frameworks. This approach is clearly manifesting an attempt to reconcile regulatory uniformity with political limitations on deeper harmonisation. It aims to be a transition towards a legal framework specifically designed to more effectively facilitate cross-border activities in Europe. It goes hand in hand with the argument that before venturing into the global market, European companies should prioritise strengthening their presence within Europe.

Capital Markets as a Stress Test: From Free Movement to SIURegarding the freedom of capital, primary EU law is particularly liberal. Article 63 of the Treaty on the Functioning of the European Union (TFEU) prohibits all restrictions on capital movements within the EU and between Member States and third countries. The CJEU has even interpreted EU law on capital and payments in a dynamic way that reinforces its role as a central pillar of market integration (Samaras, 2022). Even so, further provisions in the TFEU stipulate a number of exceptions to the principle of free movement of capital. Article 65 TFEU stipulates derogations related to taxation, prudential supervision of financial institutions, public policy and public security.

The free movement of capital is enshrined in primary EU law, but in practice it relies largely on trust in banks, institutions, and the country’s economic performance.

Sometimes the implementation of the free movement of capital lacks certainty. As an example, one might cite the experience of “capital controls” in Cyprus (2013-2015) and in Greece (2015-2019) over the past decade, as it provides a picture of the realistic limits of legal integration within the Single Market under conditions of economic turmoil and financial crisis. The free movement of capital is enshrined in primary EU law, but in practice it relies largely on trust in banks, institutions, and the country’s economic performance. When that trust is broken, exceptions become the norm.

Today, although no comparable emergency capital controls are in place in the Member States, the free movement of capital within the EU is still not fully utilised. Capital markets provide a clear test of the limits of the current integration model.

The gradual process of further liberalising the Single Market is not always linear. Naturally, the banking and financial sector’s stability has been prioritised during periods of severe crisis. Exceptional measures have been adopted in the past, in line with EU law. Consequently, the EU’s economic freedoms are not absolutely guaranteed in perpetuity, regardless of the state of the Member States’ domestic economies and the solutions offered by the EU at the time. Even the most liberal Treaty freedom operates within institutional, financial and crisis-management constraints. Today, although no comparable emergency capital controls are in place in the Member States, the free movement of capital within the EU is still not fully utilised.

Capital markets provide a clear test of the limits of the current integration model. Successive CMU initiatives have addressed several layers of capital-market integration, including prospectus rules, securitisation, long-term investment funds, company disclosure through the European Single Access Point (ESAP), trading transparency, listing rules and withholding tax procedures.[1] Yet these measures have not removed deeper structural fragmentation in supervision, insolvency law, taxation, market infrastructure and growth-stage finance.

This means that companies and investors face higher transaction costs and legal uncertainty when operating across borders. The European Commission has identified these frictions as key impediments to the effective functioning of capital markets and to the broader objective of financing growth within the EU (European Commission, 2020b). Recent analysis indicates that the main obstacle to deeper capital market integration lies in the limited centralisation of supervisory powers at EU level, with the European Securities and Markets Authority (ESMA) still lacking the authority required to ensure consistent application of rules across Member States (Gortsos, 2026).

More integrated capital markets support private risk sharing across Member States, improve the allocation of capital and enhance the resilience of the euro area to asymmetric shocks.

The European Central Bank (ECB) has also noted the macroeconomic importance of capital market integration. More integrated capital markets support private risk sharing across Member States, improve the allocation of capital and enhance the resilience of the euro area to asymmetric shocks (European Central Bank, 2024). Fragmentation reduces these benefits, it reinforces reliance on bank-based financing and constrains access to risk capital, particularly for innovative and high-growth businesses. The CMU agenda has addressed some of these issues through targeted legislative initiatives, facilitating cross-border investment and promoting supervisory convergence. Nevertheless, structural differences in national frameworks are still problematic in a cross-border context.

The initiative for a SIU, presented by the European Commission in March 2025, suggests a recalibration into a holistic approach that incorporates the entire EU financial system, attempting to mobilise European savings more effectively and to channel them into productive investment within the EU.

The initiative for a SIU, presented by the European Commission in March 2025, suggests a recalibration into a holistic approach that incorporates the entire EU financial system, attempting to mobilise European savings more effectively and to channel them into productive investment within the EU (European Commission, 2025d). It is designed to transform the foundational work of the two main CMU Action Plans (i.e. the pioneering 2015 CMU Action Plan and the 2020 CMU Action Plan), along with the parallel efforts to develop the Banking Union, into a high-impact, more inclusive and citizen-focused, financial engine. This is closely linked to concerns about the EU’s investment gap and the need to finance large-scale transitions, including digitalisation and decarbonisation (Draghi, 2024).

Towards a results-oriented EU governance approachThe governance of the Single Market is based largely on decentralised implementation.

The governance of the Single Market is based largely on decentralised implementation. Member States are responsible for applying EU law, while the European Commission -acting as the “guardian of the Treaties”- monitors compliance and initiates enforcement when required. It is unavoidable that structural challenges and disputes rise from time to time, since the application of EU law varies in practice across the 27 EU Member States. The infringement procedure against a Member State that fails to implement EU legislation remains a crucial enforcement tool. However, despite its usefulness, it addresses specific Member State breaches of EU law, not systemic patterns of violations. The Commission has framed enforcement as a strategic and preventive function, rather than merely a reactive infringement mechanism, with particular emphasis on own-initiative investigations, incorrect transposition of directives, and infringements that obstruct fundamental freedoms or the effective functioning of the Single Market (European Commission, 2022).

…the main challenge for the EU continues to be ineffective governance.

The completion of the Single Market also requires a credible delivery framework that combines, other than political commitment, a coherent legislative package and clear timelines (Jacques Delors Institute, 2026). Recent EU initiatives point towards a more targeted and measurable enforcement strategy. The “2026 Annual Single Market and Competitiveness” report introduces the first annual “Single Market Enforcement Agenda”, focused on priority barriers such as late payments and obstacles in construction and installation services linked to the green transition, while simplification packages seek to reduce administrative burdens and make Single Market rules easier to apply in practice (European Commission, 2026). Nonetheless, institutional limits hinder enforcement. Coordination mechanisms rely on cooperation and do not always generate strong incentives for compliance. Consequently, the main challenge for the EU continues to be ineffective governance.

A turning point appears to be marked by more recent developments towards a results-oriented EU governance approach. The joint “One Europe, One Market” roadmap, agreed in late April 2026 between the European Parliament, the Council and the Commission, seeks to introduce a structured implementation framework through priority legislative deliverables and clear timelines, as well as regular monitoring through quarterly stocktaking. Europe’s fragmentation was translated into a structured work programme built around five priorities: simplifying rules, deepening Single Market integration, strengthening trade, reducing energy prices while advancing decarbonisation, and driving the digital and AI transformation, supported by more than forty legislative and policy deliverables.

The roadmap shows the political commitment of the EU institutions for setting out concrete steps towards a more operational Single Market governance (Council of the European Union, 2026). It converts a broad competitiveness agenda into a delivery test: capital markets, energy, digital infrastructure and industrial policy are placed within one political framework, with timelines that make delays more visible and politically costly (Letta, 2026a).

{kind=link}

FIGURE 2: “One Europe, One Market” roadmap (April 2026), from political commitment to measurable delivery

The roadmap’s “market integration and supervision package” is particularly relevant in this respect, since the Commission’s December 2025 proposals seek to address capital-market fragmentation through changes to trading, post-trading, asset management and ESMA supervision, confirming that the SIU depends not only on new rules but on a more integrated supervisory architecture (European Commission, 2025e).

Policy RecommendationsCompleting the Single Market requires targeted action. The adoption of these strategic priorities is strongly encouraged:

- Target harmonisation and implementation where fragmentation is structural: EU legislative action should focus on areas such as insolvency, taxation procedures and other market obstacles, where national discrepancies create permanent barriers. Where the Treaty basis allows it, regulations may be more effective than directives, since they reduce transposition delays and limit divergent national implementation. Moreover, the Commission should track the implementation of major Single Market initiatives early, using detailed guidance and reporting to prevent new fragmentation from emerging. Attention should be paid to reducing “gold-plating” (adding extra layers of rules at the national level), which often increases compliance costs without clear policy justification.

- Reinforce supervisory convergence in capital markets: As has been pointed out in the Draghi Report (2024), the EU lacks a single securities market regulator. The ESMA ought to be transformed to serve as the sole common regulator for all securities markets within the EU. The EU should strengthen convergence through the ESMA, reinforcing transparency and technical standards, attaining a more unified supervision of capital markets.

- Constitutional discipline for restrictions on capital movements: Past episodes of capital controls show that EU law can accommodate emergency restrictions on capital movements where they are justified, proportionate and temporary. The unresolved issue is institutional. These safeguards have operated mainly through ad hoc assessment and monitoring, rather than through a permanent framework designed to protect capital-market integration. The EU should therefore develop, first through secondary legislation and eventually through Treaty reform, a stricter constitutional discipline for the use of Article 65 TFEU. Its provisions should not be abolished, since taxation, prudential supervision and public policy/security remain legitimate public interests. Its invocation, however, should be tied to clearer EU-level conditions: notification, time limitation, strict periodic review and consistency with the objective of capital-market integration. The aim would not be to invent new legality criteria, but to make their application more predictable, reviewable and aligned with the completion of the SIU.

Eliminating internal obstacles across the EU is essential for enabling market dynamics to operate effectively on a large scale.

In 2024, the findings and recommendations of the Letta and Draghi reports had been met with widespread enthusiasm (Kritikos, 2024). Eliminating internal obstacles across the EU is essential for enabling market dynamics to operate effectively on a large scale. A true unified market is needed, ensuring that conducting business between Vilnius and Madrid is as seamless as it is between Athens and Thessaloniki. The competitiveness debate is therefore also a debate about scale. The EU’s difficulty is that companies, banks and capital markets are primarily organised around national markets. In a global economy shaped by continental-scale competitors from the United States and China, the relevant benchmark is whether businesses in the EU can achieve sufficient growth to establish themselves as truly European entities, rather than remaining confined to national prominence. This does not alter the fact that slow convergence may be insufficient in sectors where technological cycles and global competition move faster than EU implementation.

A more integrated Single Market needs rules that are clear and sufficiently uniform to support cross-border growth, while avoiding unnecessary procedural burdens that make compliance easier for incumbents than for new entrants.

A more integrated Single Market needs rules that are clear and sufficiently uniform to support cross-border growth, while avoiding unnecessary procedural burdens that make compliance easier for incumbents than for new entrants. National regulatory discretion may protect domestic dominant players and, possibly, reduce unwanted competitive pressure from other Member States. This might explain why many barriers still exist even when their aggregate cost to the EU economy is widely recognised. Completing the Single Market requires confronting the domestic interests that benefit from partial integration.

A functioning SIU should be assessed by whether it enables European firms to grow within Europe, rather than pushing them towards capital markets elsewhere.

Greater scale should not be understood as a goal only for large Member States or large firms. Smaller Member States and SMEs may benefit most from a genuinely integrated Single Market, because domestic scale is structurally limited. Deeper integration can expand their addressable market and create more credible paths from local innovation to European growth. Besides, Europe does not lack startups or entrepreneurial talent, but many firms face a financing and market-size ceiling once they move from creation to scaleup. A functioning SIU should be assessed by whether it enables European firms to grow within Europe, rather than pushing them towards capital markets elsewhere.

Recent EU policy developments set out the way forward regarding greater regulatory uniformity and less economic overreliance on third countries. This direction addresses important aspects of the problem. However, legal convergence does not automatically produce effective integration. The central challenge is mostly operational, since the EU has demonstrated its ability to identify barriers and design policy responses. Ensuring consistent implementation across Member States is more difficult. The long-term political sustainability of the Single Market depends also on ensuring that mobility remains a choice rather than an obligation. As emphasised in recent policy debates, deeper integration must be accompanied by economic and social cohesion in order to remain politically viable (Letta, 2026b).

Completing the Single Market should be understood not only as an economic reform, but as a condition for European resilience and sovereignty.

The link between competitiveness and European security is also central to the Single Market debate. In a global economy, fragmentation weakens the EU’s capacity to invest, innovate and act strategically. Completing the Single Market should be understood not only as an economic reform, but as a condition for European resilience and sovereignty (Letta & Lamy, 2026). It is time for the EU to compete with the dominant players, benefitting from a higher degree of autonomy by boosting its economy. For the EU this requires a decisive shift from agenda-setting to delivery. It implies departing from mediocrity, with stronger enforcement, greater administrative capacity and sustained political commitment.

Completing the Single Market means making Europe the natural scale of economic activity, rather than leaving firms, capital and innovation trapped in national markets.

From the early stages of the internal market, European policymakers recognised that incomplete integration risks reducing the market to a form of managed openness instead of a fully functioning economic space (European Commission, 1985). The struggle over the same strategic choice is still relevant today. The key question is whether Europe can transition from a culture of national protectionism to a European-scale mindset. Completing the Single Market means making Europe the natural scale of economic activity, rather than leaving firms, capital and innovation trapped in national markets.

ReferencesAarnio, R., Bogucki, A., Jorge Ricart, R., Timmers, P., & Vainio, T. (2026). Building One Europe, One Market: Four strategic priorities for the digital single market (Sitra Studies 258). Sitra.

ANA-MPA. (2026a, March 17). Pierrakakis at Euronext: SIU will boost job quality across Europe. https://www.amna.gr/mobile/article/978705/Pierrakakis-at-Euronext-SIU-will-boost-job-quality-across-Europe

ANA-MPA. (2026b, May 13). Pierrakakis: We need greater integration in Europe, bank mergers, larger businesses. https://www.amna.gr/article/992554/pierrakakis-we-need-greater-integration-in-europe–bank-mergers–larger-businesses

Andrews, D., Turban, S., & Tyros, S. (2026). Regulatory compliance costs and productivity: New task-based evidence (OECD Economics Department Working Papers No. 1856). OECD Publishing. https://doi.org/10.1787/1c1da52e-en

Capuano, V. (2025). New legislative approach with old legislative tools: The recent (ab)use of regulations in European Union law. Eurojus, 4, 145–163. https://rivista.eurojus.it/new-legislative-approach-with-old-legislative-tools-the-recent-abuse-of-regulations-in-european-union-law/

Council of the European Union. (2026). One Europe, One Market Roadmap of the European Parliament, the Council of the European Union and the European Commission (ST-8473/26).

https://data.consilium.europa.eu/doc/document/ST-8473-2026-INIT/en/pdf

Court of Justice of the European Union. (2026). Annual report 2025: Statistics concerning the judicial activity of the Court of Justice. https://curia.europa.eu/site/upload/docs/application/pdf/2026-05/ra_en_court_statistiques_25.pdf

Draghi, M. (2024). The future of European competitiveness. European Commission. Part A: https://commission.europa.eu/document/download/97e481fd-2dc3-412d-be4c-f152a8232961_en; Part B: https://commission.europa.eu/document/download/ec1409c1-d4b4-4882-8bdd-3519f86bbb92_en?filename=The%20future%20of%20European%20competitiveness_%20In-depth%20analysis%20and%20recommendations_0.pdf

European Central Bank. (2024). Financial integration and structure in the euro area. https://www.ecb.europa.eu/press/fie/html/ecb.fie202406~c4ca413e65.en.html

European Commission. (1985). Completing the internal market: White paper from the Commission to the European Council (Milan, 28–29 June 1985) (COM(85) 310 final). https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:51985DC0310

European Commission [Directorate-General for Internal Market, Industry, Entrepreneurship and SMEs & Centre for Strategy & Evaluation Services]. (2015). Cost of the cumulative effects of compliance with EU law for SMEs: final report. Publications Office. https://data.europa.eu/doi/10.2873/554243

European Commission. (2020a). Identifying and addressing barriers to the Single Market (COM(2020) 93 final).

https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:52020DC0093

European Commission. (2020b). A Capital Markets Union for people and businesses: New action plan (COM(2020) 590 final).

https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:52020DC0590

European Commission. (2022). Enforcing EU law for a Europe that delivers (COM(2022) 518 final).

https://commission.europa.eu/publications/communication-commission-enforcing-eu-law-europe-delivers_en

European Commission. (2024). The 2024 Annual Single Market and Competitiveness Report (COM(2024) 77 final). https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:52024DC0077

European Commission. (2025a). A Competitiveness Compass for the EU (COM(2025) 30 final). https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=celex:52025DC0030

European Commission. (2025b). The Single Market: Our European home market in an uncertain world (COM(2025) 500 final). https://single-market-economy.ec.europa.eu/publications/single-market-our-european-home-market-uncertain-world_en

European Commission. (2025c). Startups, scaleups and entrepreneurship. [Flash Eurobarometer 559]. https://europa.eu/eurobarometer/surveys/detail/3359

European Commission. (2025d). Savings and Investments Union: A strategy to foster citizens’ wealth and economic competitiveness in the EU (COM(2025) 124 final). https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:52025DC0124

European Commission. (2025e). Market integration and supervision package. https://finance.ec.europa.eu/publications/market-integration-and-supervision-package_en

European Commission. (2026). The 2026 Annual Single Market and Competitiveness Report (COM(2026) 46 final).

https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=COM:2026:46:FIN

European Council. (2026). European Council conclusions, 19 March 2026.

https://www.consilium.europa.eu/en/meetings/european-council/2026/03/19/

European Court of Auditors. (2026). Single market for services: Commission action to remove barriers to cross-border services still insufficient (Special Report No 13/2026). https://www.eca.europa.eu/en/publications/SR-2026-13

Gortsos, C. (2026). European (EU) capital markets law at (close to) 50: Historical evolution and missing elements (EBI Working Paper No. 207). European Banking Institute. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=6689178

Hallak, I. (2026, April). The 28th regime corporate legal framework (PE 785.710). European Parliamentary Research Service, European Parliament. https://www.europarl.europa.eu/thinktank/en/document/EPRS_BRI(2026)785710

IMF. (2024, October). Regional Economic Outlook for Europe: A Recovery Short of Europe’s Full Potential.

Jacques Delors Institute. (2026). One Europe, One market: Europe’s strongest response to a world in transformation. https://institutdelors.eu/content/uploads/2026/04/One-Europe-One-Market_paper_v3-1.pdf

Kammer, A. (2025, June). Europe’s integration imperative. International Monetary Fund. https://www.imf.org/en/publications/fandd/issues/2025/06/europes-integration-imperative-alfred-kammer

Kritikos, A. (2024). The Letta and Draghi reports: The only way to go, despite the hurdles (European Economy Policy Briefs No. 5/2024). Hellenic Foundation for European and Foreign Policy (ELIAMEP). https://www.eliamep.gr/wp-content/uploads/2024/11/Policy-briefs-special-edition-Leventis-5-EN-.pdf

Letta, E. (2024). Much more than a market. Council of the European Union.

https://www.consilium.europa.eu/media/ny3j24sm/much-more-than-a-market-report-by-enrico-letta.pdf

Letta, E. (2026a, May). One Europe, One Market Roadmap: Building Europe’s capacity to act. Centre for Economic Policy Research. https://cepr.org/system/files/publication-files/299775-one_europe_one_market_roadmap_building_europe_s_capacity_to_act.pdf

Letta, E. (2026b, February 26). One Europe. One market. Time to complete the EU single market. Politico. https://www.politico.eu/article/time-complete-eu-european-single-market-next-step/

Letta, E., & Lamy, P. (2026, March 17). Now more than ever, Europe must complete the Single Market. Project Syndicate. https://www.project-syndicate.org/commentary/eu-completing-single-market-key-to-defense-energy-security-tech-sovereignty-by-enrico-letta-and-pascal-lamy-2026-03

OECD. (2025). Better Regulation Practices across the European Union 2025. OECD Publishing. https://doi.org/10.1787/6f007516-en

Publications Office of the European Union. (n.d.). Legal acts – statistics. EUR-Lex. https://eur-lex.europa.eu/statistics/legislative-acts-statistics.html

Samaras, A. (2022). Οι κεφαλαιακοί περιορισμοί στο σύγχρονο ενωσιακό δίκαιο [Restrictions on the free movement of capital in contemporary EU law]. Nomiki Bibliothiki.

Thomadakis, A., & Marcus, J. S. (2025). Identification of hurdles that companies, especially innovative start-ups, face in the EU justifying the need for a 28th regime (PE 775.947). European Parliament, Policy Department for Justice, Civil Liberties and Institutional Affairs. https://www.europarl.europa.eu/RegData/etudes/STUD/2025/775947/IUST_STU(2025)775947_EN.pdf

Wax, E., & Ionta, N. (2026, April 28). Who killed the directive? Euractiv.

https://www.euractiv.com/news/rapporteur-who-killed-the-directive/

[1] See, indicatively, Regulation (EU) 2017/1129; Regulation (EU) 2017/2402; Regulation (EU) 2023/606; Regulation (EU) 2023/2859; Directive (EU) 2024/790; Regulation (EU) 2024/791; Regulation (EU) 2024/2809; Directive (EU) 2024/2811; Council Directive (EU) 2025/50.

Categories: Diplomacy & Defense Think Tank News, Swiss News

Cette filière agricole dépasse les attentes avec une récolte abondante en 2026

Après plusieurs années d’investissements dans l’agriculture, les premiers résultats sont au rendez-vous. Les données provisoires de la campagne moisson-battage 2026 font état d’une récolte céréalière […]

L’article Cette filière agricole dépasse les attentes avec une récolte abondante en 2026 est apparu en premier sur .

Categories: Afrique, European Union

Can Girmay recreate past Tour de France glories with new team?

Biniam Girmay, who is now backed by a World Cup winner, is aiming to reclaim the green jersey two years after the Eritrean made history at the Tour de France.

Categories: Africa, European Union

Press release - Press conference on updated air passenger rights on Tuesday at 14.00

After the final vote in the European Parliament on Tuesday, key EP negotiators Andrey Novakov and Virginijus Sinkevičius will brief journalists on the EU air passenger rights rules review.

Committee on Transport and Tourism

Source : © European Union, 2026 - EP

Committee on Transport and Tourism

Source : © European Union, 2026 - EP

Categories: Afrique, European Union

Press release - Press conference on updated air passenger rights on Tuesday at 14.00

After the final vote in the European Parliament on Tuesday, key EP negotiators Andrey Novakov and Virginijus Sinkevičius will brief journalists on the EU air passenger rights rules review.

Committee on Transport and Tourism

Source : © European Union, 2026 - EP

Committee on Transport and Tourism

Source : © European Union, 2026 - EP

Categories: Afrique, Europäische Union

Press release - Press conference on updated air passenger rights on Tuesday at 14.00

After the final vote in the European Parliament on Tuesday, key EP negotiators Andrey Novakov and Virginijus Sinkevičius will brief journalists on the EU air passenger rights rules review.

Committee on Transport and Tourism

Source : © European Union, 2026 - EP

Committee on Transport and Tourism

Source : © European Union, 2026 - EP

Categories: Balkans Occidentaux, European Union

Press release - Press conference on updated air passenger rights on Tuesday at 14.00

After the final vote in the European Parliament on Tuesday, key EP negotiators Andrey Novakov and Virginijus Sinkevičius will brief journalists on the EU air passenger rights rules review.

Committee on Transport and Tourism

Source : © European Union, 2026 - EP

Committee on Transport and Tourism

Source : © European Union, 2026 - EP

Categories: Balkans Occidentaux, Európai Unió : hírek magyarul

Algérie – France : des billets Algérie Ferries à partir de 23 020 DA pour ces 2 traversées

La compagnie nationale Algérie Ferries a annoncé le lancement d’une nouvelle offre promotionnelle exceptionnelle destinée aux voyageurs souhaitant rejoindre la France cet été. Cette promotion […]

L’article Algérie – France : des billets Algérie Ferries à partir de 23 020 DA pour ces 2 traversées est apparu en premier sur .

Categories: Afrique, European Union

Discounting Demographic Realities

Rather than adapting to persistent low fertility, population ageing, and slower labor-force growth, many governments continue to pursue policies aimed at reversing these trends and restoring demographic conditions more characteristic of the mid-20th century. Credit: Shutterstock

By Joseph Chamie

PORTLAND, USA, Jul 3 2026 (IPS)

Demographic realities are well documented, and governments have long been aware of the profound demographic changes now underway. Nevertheless, many policymakers continue to discount or ignore these demographic trends.

This reluctance often reflects the tension between short-term political priorities and long-term demographic realities. As a result, governments are frequently unwilling to acknowledge the full scale of the major demographic transformations reshaping their societies.

In some cases, demographic denialism serves to protect entrenched political or economic interests. More often, however, it reflects an unwillingness to confront politically difficult policy choices, such as raising taxes, expanding immigration, increasing retirement ages, or committing additional resources to pensions, healthcare, and other social welfare programs.

Many countries are already experiencing population decline, with deaths exceeding births. In 63 countries, home to about 28% of the world’s population, population size has already peaked. Over the next thirty years, the populations of an additional 48 countries and areas are also expected to reach their peak before entering a period of decline

Because demographic change typically unfolds gradually, politicians often prioritize policies that deliver immediate political or economic benefits over reforms designed to address long-term challenges such as population decline and demographic ageing. Electoral incentives and short-term political considerations often outweigh the need to adapt to evolving demographic realities.

Governments may also downplay demographic trends because doing so enables them to pursue short-term political priorities and ideological objectives while postponing the more difficult fiscal and policy adjustments required by demographic change.

Moreover, some policymakers continue to pursue measures intended to restore the demographic patterns of the recent past, despite the limited likelihood that such efforts will succeed.

The demographic conditions of the 20th century were historically exceptional. Population growth, fertility rates, age structures, declining mortality, and gains in life expectancy all reached unprecedented levels, particularly during the second half of the century. These conditions were the product of a unique combination of historical, economic, technological, and public health factors and are unlikely to be repeated. Rather than attempting to recreate the demographic environment of the past, governments should focus on adapting institutions, policies, and public finances to contemporary demographic realities.

The world’s population nearly quadrupled during the 20th century, rising from 1.6 billion in 1900, to 2.5 billion in 1950, and then to 6.2 billion by 2000.

Today, the global population is approximately 8.3 billion, more than five times its size in 1900. Although the world’s population is expected to continue growing, the rate of growth has slowed dramatically. According to current projections, the global population is expected to peak at approximately 10.3 in the mid-2080s before declining slightly to around 10.2 billion by the end of the century (Table 1).

Source: United Nations.

The world’s population growth rate, which was 1.7% in 1950, rose to a peak of about 2.3% in the early 1960s. By the end of the 20th century, it had declined to about 1.4%. In 2026, the global growth rate is estimated at approximately 0.8% and is projected to continue decreasing, reaching about -0.1% by the end of the century.

Moreover, many countries are already experiencing population decline, with deaths exceeding births. In 63 countries, home to about 28% of the world’s population, population size has already peaked. Over the next thirty years, the populations of an additional 48 countries and areas are also expected to reach their peak before entering a period of decline.

Fertility levels have also fallen dramatically from the relatively high levels of the mid-20th century. The global fertility rate, which averaged more than five births per woman in the late 1950s, had declined to about half that level by the beginning of the 21st century. By 2026, the world’s fertility rate is estimated at approximately 2.2 births per woman. Furthermore, more than half of all countries now have fertility rates below the replacement level of approximately 2.1 births per woman.

Population ageing is another defining demographic trend. In 1950, only about 5% of the world’s population was aged 65 or older. By 2026, that proportion had more than doubled to nearly 11%. The proportion of the population aged 85 and older has increased even more rapidly, rising from just 0.2% in 1950 to about 1% in 2026.

As populations age, people are also living longer than ever before. Global life expectancy at birth has increased substantially, from about 46 years in 1950 to approximately 74 years in 2026.

Life expectancy at age 65 has also risen substantially. Globally, it increased from about 11 additional years in 1950 to approximately 18 additional years by the mid-2020s. In many countries, however, the gains have been greater, with life expectancy at age 65 exceeding 20 years. In Japan and France, for example, a 65-year-old can expect to live approximately 23 additional years (Figure 1).

Source: United Nations.

Rather than adapting to persistent low fertility, population ageing, and slower labor-force growth, many governments continue to pursue policies aimed at reversing these trends and restoring demographic conditions more characteristic of the mid-20th century.

In many low-fertility countries, governments have devoted substantial public resources to pro-natalist measures such as cash transfers, tax incentives, subsidized childcare, and housing assistance. While these policies may ease short-term financial constraints for families, they have generally produced only modest and often temporary increases in fertility rates.

At the same time, despite rising old-age dependency ratios and persistent labor shortages, immigration policy remains politically contentious, and, in some countries, highly restrictive. This has occurred alongside growing fiscal strain on pay-as-you-go pension systems and increasing demand for healthcare and long-term care services.

Although life expectancy continues to increase, especially at older ages, reforms such as gradually raising retirement ages, broadening the tax base, restructuring pension systems, and adapting healthcare financing have often advanced slowly because of political resistance. As a result, fiscal adjustments frequently lag behind demographic change, contributing to mounting budgetary pressures and, in some cases, greater intergenerational tension.

In some countries, political leaders have responded to inconvenient demographic trends by weakening the independence of statistical agencies, reducing funding for demographic research and data collection, firing statisticians, sidelining professional expertise, or publicly questioning well-established demographic evidence. Such actions can make it more difficult for policymakers and the public to assess demographic change accurately, evaluate policy options, and develop effective long-term responses.

Similarly, rather than modernizing public safety nets, diversifying revenue sources, or implementing gradual reforms to retirement and pension systems, many governments postpone difficult policy decisions to minimize electoral backlash. Prolonged delays, however, can undermine the long-term financial sustainability of public programs and increase the likelihood that pension and social insurance trust funds will become insolvent or require abrupt corrective measures.

Another form of political avoidance is the maintenance of restrictive immigration policies despite persistent labor shortages. In many countries, immigration has historically helped offset population decline driven primarily by sustained below-replacement fertility. Without sufficient immigration, population decline and demographic ageing are likely to accelerate in these societies.

The major demographic shifts of the 21st century – including population decline, demographic ageing, sustained below replacement fertility, increasing longevity, migration, refugee movements, and asylum pressures – are well documented and widely recognized. Nevertheless, many governments continue to prioritize efforts to reverse these trends while devoting comparatively less attention to adapting institutions and public policies to long-term demographic realities.

Rather than focusing primarily on restoring the demographic conditions of the recent past, policymakers may benefit from placing greater emphasis on adapting economic, fiscal, and social institutions to the demographic realities of the present and the decades ahead. Such an approach recognizes demographic change not as a temporary departure from historical norms, but as a defining structural feature of the 21st century that requires sustained institutional adaptation rather than attempts at demographic restoration.

Joseph Chamie is a consulting demographer, a former director of the United Nations Population Division, and author of numerous publications on population issues.

Categories: Africa, European Union

Tempo darf kein Ersatz für Demokratie sein

Die EU-Erweiterung auf dem Westbalkan ist strategisch wichtig. Doch wer den Beitrittsprozess beschleunigen will, darf Demokratie und Rechtsstaatlichkeit nicht zur Nebensache machen. Ein Beitrag von Karina Mross.

Categories: Diplomacy & Defense Think Tank News, European Union

Tempo darf kein Ersatz für Demokratie sein

Die EU-Erweiterung auf dem Westbalkan ist strategisch wichtig. Doch wer den Beitrittsprozess beschleunigen will, darf Demokratie und Rechtsstaatlichkeit nicht zur Nebensache machen. Ein Beitrag von Karina Mross.

Categories: Diplomacy & Defense Think Tank News, European Union

Tempo darf kein Ersatz für Demokratie sein

Die EU-Erweiterung auf dem Westbalkan ist strategisch wichtig. Doch wer den Beitrittsprozess beschleunigen will, darf Demokratie und Rechtsstaatlichkeit nicht zur Nebensache machen. Ein Beitrag von Karina Mross.

Categories: Diplomacy & Defense Think Tank News, European Union

Inondations en Côte d'Ivoire : plus de 50 morts, des quartiers submergés et un gouvernement sous pression

Ces nouvelles inondations qui ont frappé la Côte d'Ivoire, avec un bilan de 59 morts, rappellent la vulnérabilité du pays face aux pluies torrentielles exacerbées par les changements climatiques.

Categories: Afrique, Union européenne

Inondations en Côte d'Ivoire : plus de 50 morts, des quartiers submergés et un gouvernement sous pression

Ces nouvelles inondations qui ont frappé la Côte d'Ivoire, avec un bilan de 59 morts, rappellent la vulnérabilité du pays face aux pluies torrentielles exacerbées par les changements climatiques.

Categories: Afrique, Határon túli magyar portálok összesített hírei

Protokoll - Mittwoch, 6. Mai 2026 - Donnerstag, 7. Mai 2026 - PE788.835v01-00 - Ausschuss für Sicherheit und Verteidigung

Quelle : © Europäische Union, 2026 - EP

Categories: Afrique, Europäische Union

Pages

the old site is here

© 2012-2015 Europa Varietas Foundation © 2015-2020 Europa Varietas Association

www.europavarietas.org | info(@)europavarietas(dot)org | Switzerland

This is a GDPR ready site

We are looking for sponsors for the English translation of these books, please contact turkeandras(at)gmail(dot)com